Bangalore, the IT hub of India is one of the fastest growing cities of the country. Bangalore is the home of head offices of almost all IT companies of India. This city is better known as the pioneer of IT industry in India.

If you are one of the millions of Bangalorians then you must be convinced that how deep the technology has made its impact in our lives. The tech driven crowd of Bangalore is in a deep love of technologies. Where the people here use technology for the daily chores, how can it be possible that the financial works done here manually? The finance functioning here is mostly done with an online process especially the credit processing. The most availed credit product of Bangalorians is a personal loan. The popularity of personal loan in Bangalore has been gained because of being entirely online. Here is how to get a personal loan online in Bangalore. Search Lenders In this city, there are a number of lending institutes who are ready to provide personal loans to the needy. Some of them are nationalized banks, some are private banks whereas there is a great number of Bangalore based NBFCs too. You can find all the lenders online. All lenders here come up with responsive websites which can be visited anytime and from anywhere. On the website of the lender, you can get all the information about the personal loan you are searching for. One can even call the lender and talk to them as the contact information is always available on the website. Apply For The Loan Once you are have selected the lender, you can apply for a personal loan on their website as well as in mobile applications too. You will need to fill the basic information and your contact details and the desired loan amount. Submitting Documents The next step that has to be taken is submitting the needful documents. Your documents will never be asked to submit physically. What you need to do is upload the scanned copies of your documents onto the website of the lender. The documents that you need to submit are- 1. ID proof 2. Address proof 3. Income proof 4. Proof of employment Once you upload your documents, it would be verified by the bank officials. If the lenders find no issues with your documents, they will send you a confirmation mail. Getting A Call From The Lender Once you have successfully applied for the loan, you will instantly receive a call from the lender to get your personal details. If you fulfill the eligibility criteria for a personal loan, they send you an e-mail too. The mail will contain the message that your loan has been sanctioned. along with the loan agreement papers E-Sign The Loan Agreement Papers The loan agreement papers which you receive has to be duly signed and return back to the lender. By signing the on the loan agreement, you will prove that you are ready to follow the terms and conditions of the lender. You can send the signed copy of the loan agreement through e-mail once again The Disbursal After the lender receives the signed e-approval of the borrower, they initiate the loan disbursal process. Once the loan is sanctioned, it takes only a few hours to disburse the loan amount. The loan amount will be deposited into the bank account of the borrower. Once your bank account is credited with the loan amount, the next moment you will be able to use the fund. Because of being very fast in the processing such online personal loans are better known as instant loans. The functioning of instant loan has been made possible only because of being online. The Repayment Of The Loan Once the loan is disbursed and you have made the best possible use of it, now it comes to repay the loan. Even the repayment of the loan is done online if you have availed an online personal loan. The repayment of the loan is done by an auto debit process with the approval of the borrower. On a particular date on every month, a fixed amount of money will be debited till the repayment is completely done. Getting a loan and repaying it back comes in a hassle-free process in IT cities like Bangalore. One can easily avail personal loans online and fulfils the urgent need of money. Just being assured of enough balance on the EMI day is the thing which one has to be concerned of.

0 Comments

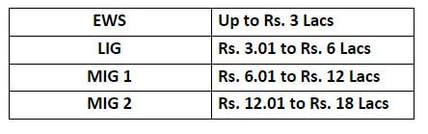

With the motto of 'Housing for All' by the year 2022, the Pradhan Mantri Awas Yojana scheme is heading towards its goal at full swing. The National Housing Bank has announced in May 2018 that a corpus of Rs 3,018 crore against 140,943 units under the credit-linked subsidy scheme (CLSS) of the Pradhan Mantri Awas Yojana (PMAY) has been dispatched till the announcement date. The Beneficiaries This scheme benefits Economically Weaker Section (EWS), Low Income Group (LIG), Middle Income Group-I (MIG-I), and Middle Income Group-II (MIG-II) of society. The divisions are done depending on the annual income of the family. Here is how the categories are made-  a) The applicant/family/household should not own a pucca house either in his name or any of his family member’s names. b) The applicant must not have availed any central/state housing subsidy under any housing scheme from Government of India ever. c) The property must be co-owned by a female member of the family d) Location of the property should fall under all statutory towns as per 2011 census and their adjacent planning area. e) The applicant's age must not be more than 70 years. f) The Applicant must be a citizen of India Eligibility Criteria For MIG

The Documents Needed To apply for subsidy under PMAY, one needs to furnish some documents. Here is the list of documents which has to be handy while applying for the subsidy.

How to Apply For PMAY? If you fulfil all the criteria of PMAY, you can definitely apply for a subsidy. The subsidy can be applied in two different ways. The first way is applying independently and the second way is to apply via bank in the case of applying a home loan subsidy. If you want to have the subsidy for building your home, you can apply for the same independently through the website of PMAY. The online application form which is available on the website has to be filled. One can download the form and fill it. On the website, one has to click on Citizen Assessment. Under the citizen assessment select 'benefit under 3 components' if you belong to EWS or LIG. After this you are to submit the 'Format-B applications. If you are a home loan borrower and want a home loan subsidy, then the subsidy is claimed through the financial institution from which the loan has been taken. After the sanctioning of the loan, the details of the borrower/applicant is verified. Once the verification is done successfully and the applicant is proved to be eligible for the subsidy, the process can be started. The subsidy claiming is done by the lending institution on the behalf of the home loan borrower, claims the subsidy. Once the subsidy is granted the amount will be disbursed by the National Housing Bank towards your loan account. The subsidy amount deducts your principal amount and hence you will have to pay a lower EMI amount. To avail of the subsidy under EWS and LIG category, the must be co-borrowed by a female member of the family. For middle-income group (MIG), one must submit Adhaar card of the applicant (s). The Updates on PMAY Scheme The rules on PMAY has undergone some upgradation recently. The scheme which has already helped a huge number of people to avail their own homes has become more convenient. Previously the GST on this scheme was of 12% which is now brought down to 8%. Any person who is buying a home for the first time will be paying GST of 8% instead of 12%. This can be a real form of an exciting news for any middle class Indian.  Loans have become an inseparable part of the life of any individual of the present generation. The one who claims to be debt free, even owns one or two credit cards in their wallet which a form of the loan itself. So, bearing a loan is no more a great thing to think about for any of us. The doorstep service of creditors has made the availing of a loan much easier, faster and hassle-free.

Though almost all loans are easy to avail, selecting the types of loan which one should avail and the one which is to be avoided is a tricky task. Every person has some needs and some wants in their lives. Sadly there is a very fine line which differentiates the needs and wants of a person's life. If a person can not define that thin line, his life may face a financial turbulence in days to come. No matter it is a need or a want, any kind of shortage of fund can be certainly fulfilled by a loan. When a borrower takes a loan for his 'wants' and later finds it difficult to repay the same, it is called as a bad loan. In the same way, when a loan is taken for a good and meaningful reason, it is called as a good loan. A good loan is availed to obtain appreciating assets like a home, property, investing in business etc. But the loans that are taken for travelling, buying gadgets etc are commonly known as bad loans. How To Differentiate Between A Good And Bad Credit?

A world without internet is almost impossible to survive at present day. The present tech driven generation is much habituated with the conveniences provided by the internet. One of such convenience given by internet is an online loan.

The lending process has gone through a massive change in last decade. The personal loan providers have adopted a whole new form lending by graduating the lending process from a conventional personal loan to an online personal loan. The emerge of online loans have brought a win-win situation for both lender and borrower. Both the parties can enjoy some kind of convenience by adopting personal loans online. Here are the benefits which a borrower enjoys while applying for a personal loan online Service Round The Clock:- If you are going to apply for loans online, you don't need to wait for the bank to open. One can avail the services of the bank round the clock even on bank holidays. May it be knowing the terms and conditions of the lender, applying for the loan, checking the loan status, or anything else related to lending can be done at any time of the day. Most of the lenders nowadays use chat bots which is always there to answer the queries of any visitor to the website. Better Comparison- Comparison among the lenders has become very easy because of the online lending platforms. The personal loan comparison can be done by visiting the website of the lender. There is always a difference in the personal loan interest rates provided by different lenders. One can check the websites of many lenders to find the best personal loan interest rates. A proper research on lenders can make a borrower find the best deal in the market. Saves Time- Online personal loans are in high demand in the present credit market as this kind of loan can be availed by utilizing very little time. An online apply for personal loan makes a person save a lot of time which one had to use in conventional loans. Being in the queue for a long time to meet the bank officials or filling up a lengthy application form etc have become the things of past. An online personal loan application is now just a few clicks away which need hardly half an hour. Perfect For Emergencies- In emergencies like a medical emergency, job loss or sudden travel, we cannot wait long for that extra fund which is needed to overcome the situation. Loans Online are the best to fight such situations as online loans are always faster in approval and disbursement. A personal loan approval is provided within a few hours of applying for the loan and the loan disbursement is done on the same day if the applicant satisfies eligibility criteria of the lender. Better Tracking of the Loan Account- An online personal loan gives the borrower a better tracking facility of the loan as compared to the conventional personal loan from bank. When you opt for an online loan, the lender gives you an access to the loan account of yours where you can check all the necessary information about the loan. One can check the outstanding balance, interest rate, EMI amount, rate of interest etc in his loan account. This facility makes the borrower track his loan in a much convenient way. Minimal Documentation- The next benefit which one can enjoy while being with an online loan is the minimal documentation. One needs to submit very few documents to avail a personal loan. The general documents which you are in need to produce should be uploaded to the website of the lender instead of submitting the same physically. This facility not only saves a lot of time and effort, it keeps your documents safe too. EMI Amount Calculation- An online loan is best for persons who like to make a budget in advance and stick to it. A personal loan online comes with an online EMI calculator which calculates and tell you the exact EMI amount. The EMI amount and the loan tenure are closely connected. If you feel that that you are not comfortable with the EMI amount, you can alter the tenure. The online EMI calculator has simplified the cumbersome and complex process of calculating EMI amount. The popularity of personal loans online is a result of the conveniences given by online loans. The online application makes us find out personal loans with low interest which is the first priority of every loan seeker. One can even apply for a loan online through loan agencies like Finance Buddha which compares the best lenders so that one can find the best suited loan in terms of interest rate and terms and conditions.  Debts have become an integral part of most of our lives. Debts help us to get a high education, own our property, meet the medical emergencies or start our own business. When debts are managed well they become the stepping stone of one's life. Debts help us to achieve our goals in the easiest way ever. When a debt is managed well it makes our life much easier. However, if that same debt is not managed well, it will come back haunting us. The general perception of debts is that they are just another name of evil. But if you change your outlook on a credit, the other side of it will come to the notice. Loans or credits come into use when you are in the highest need for money. Debts are always considered as beneficial until and unless you are disciplined with the repayment schedule. Once you miss the EMI, the situations will change in an instant. You will start getting reminder messages, e-mails or calls from the bank and in worst cases, the collection agents will start visiting you. Being in debt is not actually a very big deal for any person who has a regular cash flow. But being unable to manage the same is something which can become a stumbling block and hinder our progress. Here are some guidelines for the one who is struggling with the debt. The next few minutes spent in reading the below will definitely help you to manage your debts better. Optimize Your Debts- If you are a person who has a number of debts then this is the time when you are to sit calm and optimize your debts. Make a list of all your debts, the outstanding balance, the EMI of each credit, the interest rate etc. This will give you an overview of your credits. Knowing how much you actually owe will help you to manage your monthly budget too. One must be clear on how much has to be paid every month. Don't Miss Payments- Missing payments is the action of a borrower which turns a good loan to a bad loan. Theoretically, there is no concept of a good loan or a bad loan. It the payment habit of the borrower which makes a loan call a good or a bad loan. Let your loan be a 'normal' one instead of making it good or a bad one. Pay your EMIs every month without a fail. If the repayment amount is not fixed, be assured that at least the minimum amount has been paid. Paying your EMIs regularly will slowly but surely lead you to that ultimate day when you will be able to announce yourself as debt free. Try To Refinance- A loan refinancing means when you take a fresh loan to close one loan or more than that at a time. A loan refinance is done when a person has a number of loans and he is getting it difficult to manage all. The best way to handle this type of scenario is to take a loan which is equivalent to the total outstanding amount of all loans. By doing this, one will close all the previous credit accounts. A refinance will make a borrower pay a single EMI instead of paying EMIs of a different amount to different lenders on different days of the month. Live Within Your Means- When you are in debt and your monthly outgo of paying EMIs is more than 50% of your net monthly income then you are to understand that you are in an alarming financial situation. When you are left with only 50% of your income to run the family, you should be economical while spending your money. One must be able to differentiate between 'needs' and 'wants'. Eliminating all the wants from the purchase list and focusing on the wants will make you save some amount every month. Savings should never stop, doesn't matters the amount of debt you have at any point of time. Saving will not only be needed for the emergencies, in long run this will help you to prepay your loan too. Decide Which Debt to Pay First- Every credit comes at different price or tenure. As mentioned earlier, one must optimize the debts to find out the costliest one. Once you find out which loan is costing you more, you can work towards closing that particular loan. This will omit one credit from your credit list and make you take a step towards being debt free. Credits should be taken only when it is actually needed. A loan is considered as life saviour aid when you take it for a genuine reason and you are capable of paying it back. Taking a loan and paying it regularly not only helps you to achieve your goal, it also enhances your creditworthiness for the next loan.  Marriage is one of the most special moments of a person's life. Such moments make a lifetime impression in one's life. Such moments must be lived in such a way that one has not to regret after a few years thinking that he/she could have done something more to make that moment an unforgettable one. A prime venue, flavorsome food,ornaments, gifts, dresses, honeymoon etc turn a normal wedding to a grand wedding. Every couple dreams to have a grand wedding which will be remembered by them and their friends and families for many years. But the thing to think is that such big fat marriages come at a high cost. All marriage plannings in India irrespective of community or location start with the financial planning. Estimating the budget or how much of money is going to be needed to make the marriage ceremony successful becomes the foremost topic of brainstorming of the parents and the couple. The finance becomes the major concern of the family. It is always advisable to arrange adequate fund which is going to be needed to make the wedding a grand one. But marriages are among such social celebrations where any unpredictable or unplanned expenses may arise for which you were not prepared. In the time when you feel that the lack of money can spoil your grand wedding, you can always ask for a monetary support. Here are some ways which to fund your grand wedding:- Personal Loan- Personal loans are probably one the best ways to arrange fund for a dream wedding. A personal loan is a multipurpose loan hence there is no bar on the usage of the money. One can use the borrowed amount for any personal purpose like marriages, travel, gifting etc. Personal loans are very handy loans as one can apply for a personal loan online too. Personal loans are also called as same day loan as such loans are very fast in processing and can be disbursed within one or two business days. Some lenders even disburse a loan within a few hours which makes it better known as quick loans or instant loans. Line-Of-Credit- A line of credit is more or less like a credit card. This way is very useful when you are not certain about the exact amount you need. The highest limit of the credit will be given to the borrower and one can use the amount in many small parts. One may never need to use the whole amount. So the amount which you have used is subject to return to the lender. Even one doesn't need to pay interest on the amount which he has not used. Loan Against Property- A loan against property is a secured loan. A secured loan is always a cheaper option than an unsecured loan like a personal loan. When you opt for a loan against property, you are to keep some of your assets as security against the loan. If the borrower declares himself unable to pay his debts, the lender auctions the collateral to refund the lent amount. In such type of loans, there is always a risk of the asset is associated. But the interest rate on such loans is lesser than unsecured personal loans. Home Loan Top-Up - A home loan top up is an option available only to the ongoing home loan borrowers. One can take a top up loan on an ongoing home loan which is generally a multipurpose loan. The amount which one can borrow depends on the FOIR of the applicant. Such types of loans are faster in processing as the lender has already verified your documents while providing the home loan. Along with being quick, such loans are always less costly as compared to a personal loan online. Credit Card- Credit cards can also fulfill the urgent need of money if you have adequate balance in it. But one must be very cautious while using a credit card as credit cards are the costliest way of borrowing. The interest rate on a credit card is much higher than a personal loan. One should use a credit card only if he/she is certain that he/she can repay the whole amount in the next month Or else one end up clearing a credit card bill with much more than which he has actually borrowed. The big day of a person's life must be celebrated in the best possible way. Money is among those resources which every person earns throughout his entire life but such special days will never return. So make your day a special one. Let money not be the obstacle. One can apply for online loans to overcome the financial problems.  A property which has an outstanding home loan on it is called the mortgaged property. It happens many a time that a house is bought on a home loan but before the loan is completely repaid to the lender, the owner of the home wants to sell the property. Most of the times such properties are sold when the borrower is unable to pay the EMIs or he/she wants to upgrade the home to a bigger one. Benefits of Buying A Mortgaged Property There are many advantages of buying a mortgaged property. A mortgaged property is always cheaper than the home which you will buy from a builder. Moreover, when you go for a mortgaged property, you will get a home which is ready to live in. One doesn't need to wait for long to occupy the home. A mortgage property has an even easier processing of home loan if you take the loan from the same lender who has given the previous loan for that property. The loan sanctioning becomes easy and smooth as the lender has already verified the property while sanctioning the previous loan. So the loan sanctioning process becomes easier and faster. Another advantage of buying a mortgaged property is that the buyer has to deal with an individual rather than a sales team. This will give a better flexibility for both seller and buyer to negotiate the price of the property. Moreover the buyer will be saved from the selling tricks which a professional sales team does to sell their product. How Can You Buy A Mortgaged Property? Many of the home buyers feel that buying a mortgaged property is a risky affair. But when the risk of buying a mortgaged property becomes void if the buyer knows the right procedure to buy a Mortgaged Property. One must be careful about the documents. The main document which one must check is the sale/purchase deed of property. The sale deed of the property confirms that the property belongs to the same person as nowadays the sale deed comes with a picture and thumb impression of the owner. Along with the sale deed, one must ask for the stamp duty and the registration documents of the property too. If the same property went through multiple ownerships, the buyer can also check the previous sale deeds to check the authenticity of the property. However, the buyer has to remember that the original documents of the home are mortgaged with the bank in order to avail the loan. Hence, the seller can only provide the photocopies of the documents. If the property is in under a housing society, one should also ask for a No Objection Certificate from the society. It may happen that the property has co-owners, in that case, the buyer should also seek for a NOC from the co-owner too. Whenever a home is purchased, there are mainly two ways to fund it. The first is when you fund it by yourself and the next is when you take a bank loan to fund your purchase which is known as Mortgage Loan. Here is how the procedure goes when the buyer pays the seller without a home loan- The first step is obtaining a letter from the bank where the property is mortgaged. The letter will say the exact amount which is outstanding on the property which you want to purchase. The bank will give you a certain time frame within which you are to pay that amount to the bank so that bank can close the loan. Once the loan is closed, the original property documents will be released. The buyer will pay the rest of the amount directly to the seller. As mentioned above, the bank fixes a date before which the buyer must pay the outstanding amount. Unable to pay the amount may result in paying penalty. Once the entire payment is done, the bank will issue a 'no due' certificate will proof that there is no outstanding loan on that particular property. After the clearance of loan, the original documents will be given to the owner within 5-10 working days. When the home is purchased with a home loan- One can buy a mortgaged property with a home loan too. But this procedure is a bit longer as the property is already mortgaged. In order to transfer the ownership of the property, the first step is to close the ongoing loan. The seller has to pay off the loan before he sells it. The same rule will be applicable even if the buyer applies for the loan from the same lender. A loan can never be transferred. First, the ongoing loan has to be closed and then only the next loan on the same property can be applied. The seller can pay off the outstanding loan with the downpayment which he/she will get from the buyer. Once you obtain the original document from the bank, the buyer can apply for a home loan. The application will be treated as a fresh loan and the all the criteria for the loan will be checked by the lender once again. The current mortgage rates and the processing fee will be applicable to this loan. It is true that buying a mortgaged property may be a tricky and tedious process, but if you can overcome all those hassles, it would definitely proof to be your best investment ever.  To the delight of all school kids and their parents, the summer vacation of 2018 has arrived once again. The swimming classes, skating training, crash courses are what one always enjoys throughout this high-temperature season. But for a change in the routine of both the children and the parents, this summer one can have a trip to abroad within a low budget.

Most of the people have a perception that foreign trips are very expensive but in reality, all trips to abroad are not so expensive. One can easily plan a trip to abroad with family within a budget. Here is a list of 4 budget friendly holiday destinations where you can spend a week of summer holidays. 1. Oman The first budget friendly holiday destination which occupies the top position in our list is the Oman with Muscat at its capital which is famed for being the second best city in the world. This country is in the Persian Gulf and the climate of this place is of tropical climate. The airfare of this country is around INR 18,000. Low cost staying options are available here which starts at INR 2000. One can use shared cabs for an inexpensive travelling option. To the surprise of many travellers, one can get foods like shawarma, rotisserie chicken, rice and kebabs within INR 100. 2. United Arab Emirates (UAE) Just three to four hours of air travel can land you in one of the most developed countries which we call as UAE. Dubai in UAE is the most precious tourist jewel. The air ticket generally starts from INR 15,000 which varies according to different times of the year. The stay at Dubai cost approximately INR 2000/ night. One can have food in Dubai at all the ranges. One can have budget friendly meals or can have the most expensive ones with a royal treatment too. One can plan a Dubai trip within INR 50,000 per head. 3. Malaysia In climatic perspective, Malaysia may be the best destination to visit this summer. The turquoise waters, stunning beaches and pleasant climate are always appealing when you are a traveler from a tropical country. Malaysia is one of the major tourist hubs in Asia. The round ticket to Malaysia costs around INR 20,000 for a person. Here you can get the cheapest guest houses or dormitory rooms in Kuala Lumpur starting for as low as INR 300 per night. There are many tourists spots which you can visit on a Malaysian trip. Some of these are- Kuala Lumpur, Sarawak, Pangkor, Redang Island, Elephant Orphanage Sanctuary, Chinatown Trishaw night tour. An average cost of INR 40,000 is fair enough for a person. 4. Singapore Singapore is a small Asian country which is famous for its colourful culture. The air ticket to this country comes somewhere within INR 11,000 to INR 20,000. One can stay here is traveller hostels which offers night stay at INR 600 onwards or one can go for a decent hotel for almost INR 2000/per night. The average food expense for one meal here is INR 500. The most famous tourist spots are Underwater world, Dolphin Lagoon, National Museum of Singapore etc. But the most exciting one is the day excursions or Singapore cruises which one should never miss. The travel expense for 4 Days and 3 Nights at Singapore costs around INR 42,000 per head. These all four travel destinations beyond the boundaries are below INR 45,000 which is affordable for many of us. If you find yourself in a short of some amount you can have many options to fund it. One can use a credit card, loan against security or an unsecured travel loan too. A credit card expense comes costlier than any other kind of loans if you can not pay the credited amount in that same month. One can avail a secured loan if he has any such valuables to use as collateral. If not so, one can easily avail personal loan which is faster, secure and hassle-free. There are many reasons which make a personal loan the best option to finance a travel. One can apply for a personal loan online too which is better known as online loans. Such personal loans can be applied without any physical documents. The repayment of a personal loan can be done in easy EMIs which minimize the burden of repaying it all together which happens in case of a credit card loans. If you are thinking that you are too late to plan for the trip then you are wrong. If you apply for a loan today, the amount will be credited to your bank account within 72 hours. So book your tickets, pack your backpack and set out for a stunning summer holiday at abroad.  Children are just another name of the bunch of happiness that comes to one person and changes his entire life. From the very first day of your baby in your arm to till he becomes self-dependent, it is the sole responsibility of the parents to nurture her, educate her and give her a gift of better future.

A better future for one's child is a dream of every parent. But chasing that dream needs lots of pre-planning and perseverance. All your plans regarding your children or your child's dream for his future takes a halt when it comes to the finance. A proper financial planning must be done at an early age of your child so that the dream of your child can come into reality without any financial hiccups. Why A Financial Planning Is Needed For Your Child's Better Future? As long as your child is undergoing primary education, you may not feel the financial pressure. The time when you are with a less pressure is the best time to make yourself prepared for the days when you will need to invest a lot in your child's education. As the inflation of money makes its highest effect on the education sector, it is almost unbelievable that the higher education is going to cost a sky-high amount. For example, the 2018 batch of IIM Ahmedabad has to pay a course fee of INR 19.5 lakhs for a two years course which is 400% higher than the course fee of 2007. This shocking fact may make the parents stand speechless thinking about the corpus which they will need for higher education of their child. Let's say your child is now 3 years old. He will go to college after 15 years. At present day the college expense of one student is around INR 5 lakhs. If we take inflation at 10%p.a., it will cost around INR 20.88 lakhs after 15 years when he will go to college. How Should You Plan? After 15 years when this big day of admitting your child to college will come, you must not struggle to arrange this fund. If one starts saving early then he can easily bear the expense. Assuming a return of 12% pm, one has to invest Rs.4180 per month so that he can have a return of Rs.20 lakhs. This is just an example of a general graduation. If one goes for professional courses, It would cost much more. According to the course fee and the age of the child, one has to calculate the investment. An investment is always sooner is better. The ideal investment for your child's higher expense should start when your child has stepped the school premises for the first time. When you start investing at an early age, you can attain your financial goal at a comparatively lower investment and of course lower physiological pressure. The best way to start investing is with a mix of different kind of investments. One must not invest in only one platform. Some of the secured government securities such as National Savings Certificate, NSC, and Public Provident Fund, PPF are a must have as though they give a low return but they are certain. While one should have some investments in mutual funds and primary equity markets too for a higher return. The secured investments will reduce the risk while the rest comes with a probability of higher returns. While investing in mutual funds, the best returns can be expected when the investment gets a hike along with the growing income. If a person makes a hike of a minimum of 20% in his SIPs every year, he will be able to earn a return of almost double which he will get with a uniform SIP whole through the tenure. Points To Ponder Before Investing

|

Categories |

RSS Feed

RSS Feed